| |

American Survival Newsletter:

Combining the World of Finance, Health & Politics

8/2/13

|

|

American Gold

A weekly newsletter brought to you by

Discount Gold & Silver 800-375-4188

Edited by Alfred Adask

Friday, August 2nd, A.D. 2013 |

|

| |

| MARKETS |

| |

Between Friday, July 26th, and Friday, August 2nd, the bid prices for:

| Gold fell 1.5 % from $1,333.80 to $1,313.50 |

| Silver fell 0.5 % from $19.99 to $19.89 |

| Platinum rose 1.3 % from $1,427 to $1,445 |

| Palladium rose 0.7 % from $725 to $730 |

| DJIA rose 0.6 % from 15,558.83 to 15,658.36 |

| NASDAQ rose 2.1 % from 3,613.16 to 3,689.59 |

| NYSE rose 0.7 % from 9,620.13 to 9,690.07 |

| US Dollar Index rose 0.3 % from 81.66 to 81.93 |

| Crude Oil rose 2.1 % from $104.64 to $106.83 |

|

|

| |

|

|

"Only buy something that you'd be perfectly happy to hold

if the market shut down for 10 years."—Warren Buffett

“If the market shut down for 10 years, what investment would you

dare to hold—other than gold?”—Alfred Adask

|

|

Pension Panic

by Alfred Adask

City of Detroit

On July 18, Detroit’s $18.5 billion bankruptcy became the largest U.S. bankruptcy ever. (OK, not “ever,” but “so far”.)

The Detroit Free Press (“Detroit: Snapshot of a City in Trouble”) described the bankruptcy as marred by “legal wrangling . . . that will involve more than 100,000 creditors, which include the Police and Fire Retirement System and the General Retirement System and its 20,000 retirees.”

Detroit’s emergency financial manager Kenneth Orr offered government retirees some temporary relief, promising:

"We have made a decision that for the balance of this year, the next six months, we're not touching pension or health care. So all pensioners, all employees you should understand: It's status quo for the next six months."

Yay! The former Detroit government employees will continue to receive their pensions for the next six months!!!!

But, after that, Katie bar the door.

How’d you like to be retired, dependent on your pension to support you for the rest of you life, and learn that your pension payments were only guaranteed “for the next six months”? How different is six guaranteed months of pensions from a doctor’s “guarantee” to a terminally-ill patient that he has got six months to live? Would either “guarantee” be cause for celebration or despair?

“Orr has not yet specified the cuts to pensions he will seek through the bankruptcy process. He has proposed freezing pensions and moving workers to a 401(k)-style plan to help alleviate the pension systems' unfunded liabilities of $3.5 billion [almost 20% of the City’s total debt]. He also wants to move retirees to Medicare or health care exchanges being set up through the Affordable Care Act.”

Thus, part of Detroit’s bankruptcy plan is to dump city retirees’ health care costs on the feds.

Michigan Governor Rick Snyder said Detroit had reached “the end of the line”; that the city was “done in” by 60 years of “residential and business flight to the suburbs, loss of its manufacturing base, chronic overspending and mismanagement and corrupt leadership, all reaching a climax as the economic meltdown and the national housing crisis hit.”

In essence, the people of Detroit have seen their lives ruined by 60 years of big and bad government. That’s why Detroit—which, in A.D. 1950, was America’s 5th largest city with a population of 1.8 million—is today America’s 18th largest city with a population of 700,000. In the same time that America’s population more than doubled from 150 million to 310 million, a big, bad, corrupt and greedy government helped drive over 1 million productive people (55%) out of Detroit.

• In “Virtually Unreported: Detroit's Bankruptcy Came With Sky-High Tax Rates, Not 'Small Government,'” Newsbusters agreed.

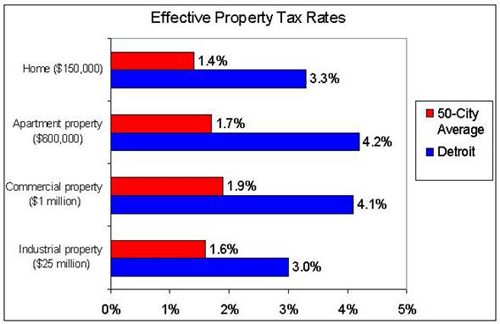

Although, “MSNBC's Melissa Harris Perry claimed that Detroit's bankruptcy is a result of ‘when government is small enough to drown in your bathtub,’ . . . The truth is that Detroit has had quite a large government, . . . frightening rates of violent and nonviolent crime, incredibly awful schools, and a race-based culture that the press once praised. What is far less appreciated is what Detroit did to chase citizens and businesses out of the city in the form of sky-high taxes. In 2012, Detroit's income tax was the highest in Michigan by far . . . . The following graph illustrates how Detroit's property tax rates compare to the average of the 50 largest other cities in the U.S.:”

Generally speaking, Detroit’s recent tax rates have been two or three times higher than the national average.

Under the leftist political and financial model of “big government,” people and businesses are expected to accept all tax increases gracefully, just follow orders, pay them, and go on with life and business as usual. But, the reality is that the people don’t accept high taxes but instead try to leave the taxing jurisdiction or simply refuse to pay those taxes.

The city government’s incompetence, corruption and mindless greed chased Detroit’s most productive private-sector members (on which the government predates or at least depends) out of the city.

Result? Detroit caved under the weight of big government—including the weight of pensions for government retirees who used to gloat over how “sweet” it was to work for the government.

Now, government retirees who once expected a lifetime of generous pensions have just six months of pension security. After that, they might receive as little as ten cents for every pension dollar due.

I guarantee that Detroit’s government pensioners won’t be gloating this time next year.

City of Chicago

According to the Chicago Sun-Times (“City of Chicago’s cash cushion plummets, debt triples, arrests drop, water use rises”), Chicago isn’t as bad off as Detroit is, but it’s not be so far behind, either.

“Last week, Moody’s Investors ordered an unprecedented triple-drop in the city’s bond rating, citing Chicago’s ‘very large and growing’ pension liabilities, ‘significant’ debt service payments, ‘unrelenting public safety demands’ and historic reluctance to raise local taxes . . . .

“Mayor Rahm Emanuel closed the books on 2012 with $33.4 million in unallocated cash on hand—down from $167 million the year before—while adding to the mountain of debt piled on Chicago taxpayers . . . . Experts recommend a cash cushion of at least $200 million for a budget the size of Chicago’s, according to the Civic Federation.

“Budget Director Alex Holt blamed the $133.6 million drop on ‘honest’ budgeting . . . .”

Omigosh! So it’s come to that, has it? Chicago’s city government is so nearly insolvent that they’ve finally been forced to resort of “honest budgeting”?!! Richard Daley and Al Capone must be rolling in their graves.

“Let’s be straightforward about what we’ve got to spend . . . . This is about matching revenues with expenses. You don’t want to over-tax people.”

Heaven forfend! Government never wants to overtax today’s voters ‘cuz that might make the voters mad enough to throw some of the crooks out of public office. However, government will go merrily borrow so much money as to leave an endless, unpayable debts for today’s children. But borrowing isn’t the same as overtaxing our children because . . . um . . . uh . . . . well actually . . . when you stop to think about it . . . leaving all those debts to future generations is overtaxing them, isn’t it?

“The new round of borrowing brings Chicago’s total long-term debt to nearly $29 billion. That’s $10,780 for every one of the city’s nearly 2.69 million residents. . . . Last year, now-retiring City Comptroller Amer Ahmad argued that the city’s debt load was not ‘troubling’ because, ‘We still have a very strong bond rating. Our fiscal position is getting better every year and we are aggressively managing our liabilities and obligations.’”

In other words, a year ago, the city government’s attitude was Why sweat the bills so long as the credit card still works? Chicago (like Detroit and the federal gov-co) expected that it could simply borrow, borrow, borrow and spend, spend, spend its way back to prosperity and economic stability.

However, today, (when City Comptroller Ahmad is going to “retire”—perhaps like a rat leaving a sinking ship) Chicago’s “fiscal position” is clearly not “getting better”. In fact, since Moody’s imposed a “triple-drop in Chicago’s bond [credit] rating,” Chicago’s access to easy credit is bye-bye.

Now what? A politician without access to credit is merely a windbag. A government without access to easy credit will be despised.

A year from now, Chicago’s “fiscal position” should be worse. At some point in the foreseeable future, the Chicago’s “fiscal position” may collapse just like Detroit’s.

“Unkeepable” Promises

It’s important to understand that it’s not “Chicago” that’s going broke—it’s the government of Chicago that’s going broke. The public confuses the city government’s debt with the people’s debt. Government, of course, wants that confusion. Government wants people to believe that its debts are their debts.

But as the people of Chicago (like those of Detroit) begin to sense that confusion, some will resist paying the city’s debts and thereby going into personal poverty and bankruptcy. Others, forced into a declining standard of living by government mismanagement will simply be unable to keep paying more taxes to support bigger and bigger government.

The result is that Chicago’s government is increasingly unable to raise taxes to pay the governments existing debt or to pay for additional debt. If government raises taxes, it’ll antagonize the city’s voters. More antagonism will lead to more tax resistance.

As government’s ability to raise taxes or borrow falls, government will be caught between the rock and the hard place. The rock is the fact that government doesn’t produce anything and therefore can’t work itself out of debt; it must rely on its residents to somehow pay its debts. The hard place is the fact that the most prosperous residents have fled, the remaining residents are too impoverished to pay government’s debts. Therefore, government can’t raise taxes or borrow enough more money to support its extravagant promises.

Result? Promises must be broken. And where will those promises be cut first? Government pensions.

If government cuts the costs of services currently provided to the people, the people might riot.

If government cuts the wages paid to current government employees, those employees may strike.

If government cuts pensions paid to former government employees, who will strike? Who will riot? Many city retirees don’t even live in Chicago anymore; they’re down in Florida or perhaps even Costa Rica and they can’t get to Chicago for a mass protest. Many of the former government workers are too elderly to riot or protest.

And who, other than former government employees will have any sympathy for retirees who lose their pensions?

The private sector won’t care because, if they do, their concern will only cause them to pay higher taxes to support the retirees. (In fact, many private-sector people would take some secret pleasure in knowing that the former government workers—who enjoyed fat pensions and early retirements—have to take it in the neck.)

Current government employees won’t stand up for former government workers because, if the former workers don’t take pension cuts, current government workers will have to take a pay cut. Can’t have that.

Thus, there’ll be little public sympathy for former government employees who suffer pension cuts and small probability of significant public protests.

Therefore, when it comes to cutting government costs, cutting government pensions is simply the best and most logical fiscal and political choice.

This isn’t news. This reasoning is exactly why the City of Chicago has failed (actually, refused) to adequately fund city employee pension funds for years.

This refusal/inability to fund city employee pension plans is why Moody’s recent report noted that Chicago’s “total fund balance at the close of 2012 was $231.3 million and that Chicago has just $625 million in ‘leased asset reserves.’ Had the city fully funded its $1.5 billion ‘actuarially required contribution’ to its four under-funded city employee pension funds in 2012 alone, ‘these two reserves would have been entirely depleted.’”

In other words, if Chicago had fully funded city pensions for just one year, the city government might’ve been bankrupt.

Well, what can’t be paid won’t be paid. The “clouty” wheels get the grease—and former city employees don’t have much clout (except with Bill Clinton who “feels their pain”).

The logic is inescapable. The easiest and most politically-acceptable way to cut Detroit and Chicago government costs is to cut former government employees’ pensions.

State of Illinois

The Associated Press (“Comptroller says she can't pay Illinois lawmakers”) reports that,

“Illinois Governor Pat Quinn cut $13.8 million for legislators' paychecks from a budget bill earlier this month, saying it wouldn't be restored until lawmakers addressed the state's $97 billion pension shortfall. He also suspended his own pay.”

Think about that.

Illinois pension problems are so severe, that Governor Quinn has suspended the pay for state legislators—and even for himself.

I’m reminded of a scene in the A.D. 1974 Mel Brooks comedy Blazing Saddles where Cleavon Little (a black man) is surrounded by an angry mob of whites, pulls his six-shooter, points it at his own head and hollers, “One more step—and the nigger gets it!” The whites backed off.

Today’s “pension follies” are becoming similarly absurd. If state legislators don’t “do something,” the Governor won’t pay himself. (Thus, “One more step—and the Governor gets it.”)

But what does Governor Quinn expect the state legislators to do? They can’t raise taxes. They can’t cut state services. They can’t borrow more money. They’re not the Federal Reserve. They can’t print money out of thin air. Therefore, they’re screwed.

“Illinois Comptroller Judy Baar Topinka said she has no choice but to withhold lawmakers' paychecks, citing a precedent-setting court case that bars her from paying state employees without a budget appropriation or court order.

“She said, a ‘serious precedent is being created,’ that was, ‘no way to run government. Threats, blackmail and inertia may be good theater, but it makes us look ridiculous . . . . It’s time for leaders to lead.’"

She’s right about the “ridiculous”. But even Comptroller Topinka seems ridiculous when she says “It’s time for the leaders to lead.”

Really? Lead where? The “leaders” in the legislature can’t raise taxes, cut services or borrow more money. So where can they lead?

I’ll tell you where they’ll lead—or at least be forced to go: back to honesty. I know that’s an uncharted and terrifying territory seldom visited by politicians—but they’ll soon have no choice but to face the truth. Politicians have made idiotic promises (pension plans) that can’t be kept. Government employees have accepted idiotic promises (pension plans) that can’t be kept. The day has arrived when the “can’t be kept” part can’t be avoided.

Guess what, kids? Contrary to daddy’s former promises, you won’t be getting a pony for Christmas.

“Illinois' unfunded pension liability is the worst in the nation because lawmakers either skipped or shorted payments to the state's five retirement systems for decades. Inaction on solving the pension problem has led to repeated credit rating downgrades . . . .”

Note that the pension promises have been ignored for decades. That means state legislators haven’t recently decided to screw over state retirees. The policy of screwing state retiree pension plans has been ongoing for decades.

What chance is there that a policy established for decades will be suddenly reversed? Not much. Government retirees are the designated sacrificial lambs.

More, the Illinois pension problem may become very interesting because, if it’s true that:

1) Illinois has the worst pension system in the nation;

2) The people of lllinois want their legislators to “do something”;

3) The legislators won’t be paid until they “do something”;

Then,

4) We will soon see if there’s anything that can be “done” to remedy the situation—or if the pension plan promises are simply irredeemable and worthless.

If Illinois legislators are forced to admit that there’s nothing they can do, the entire Illinois pension system may collapse. Those who’ve trusted their wealth to the Illinois pension plans will lose their assets. The national economy might be adversely affected.

More, we can wonder what effect an admitted collapse of the Illinois pension system might have on pension systems across the country. How many other American pensioners will see evidence that “What can’t be paid, won’t be paid,” panic, and try to escape from whatever pension plan they’re in with however much money that they can grab?

I’ll bet that Illinois Governor Pat Quinn will soon back down from his vow to withhold legislator pay until the legislators “do something”.

I’ll bet that if Governor Quinn doesn’t back down, either State judge will order him to back down, or the federal government will somehow shore up the Illinois pension plans.

But I’m also going to bet that no matter what happens, it’ll soon be common knowledge that the Illinois state pension system is about as bankrupt as the City of Detroit and as insolvent as the City of Chicago. Once that happens, people in other States will begin to realize how fragile their pension systems may be.

If so, it’s possible that the Illinois (and Chicago and Detroit) pension debacle might precipitate a “pension panic” that spreads to other parts of the USA.

The wheels are beginning to come off the government pension systems.

But even if the Detroit/Chicago/Illinois pension debacles aren’t contagious, it’s only a question of time before another pension debacle in another state or major city precipitates a “pension panic”.

Buckle up.

It Is Happening Again: 18 Similarities Between The Last Financial Crisis And Today

Michael Snyder, on July 25th, 2013

EconomicCollapseBlog.com

If our leaders could have recognized the signs ahead of time, do you think that they could have prevented the financial crisis of 2008? That is a very timely question, because so many of the warning signs that we saw just before and during the last financial crisis are popping up again. Many of the things that are happening right now in the stock market, the bond market, the real estate market and in the overall economic data are eerily similar to what we witnessed back in 2008 and 2009. It is almost as if we are being forced to watch some kind of a perverse replay of previous events, only this time our economy and our financial system are much weaker than they were the last time around. So will we be able to handle a financial crash as bad as we experienced back in 2008? What if it is even worse this time? Considering the fact that we have been through this kind of thing before, you would think that our leaders would be feverishly trying to keep it from happening again and the American people would be rapidly preparing to weather the coming storm. Sadly, none of that is happening. It is almost as if they cannot even see the disaster that is staring them right in the face. But without a doubt, disaster is coming. The following are 18 similarities between the last financial crisis and today...

#1 According to the Bank of America Merrill Lynch equity strategy team, their big institutional clients are selling stock at a rate not seen "since 2008".

#2 In 2008, stock prices had wildly diverged from where the economic fundamentals said that they should be. Now it has happened again.

#3 In early 2008, the average price of a gallon of gasoline rose substantially. It is starting to happen again. And remember, whenever the average price of a gallon of gasoline in the U.S. has risen above $3.80 during the past three years, a stock market decline has always followed.

#4 New home prices just experienced their largest two month dropsince Lehman Brothers collapsed.

#5 During the last financial crisis, the mortgage delinquency rate rose dramatically. It is starting to happen again.

#6 Prior to the financial crisis of 2008, there was a spike in the number of adjustable rate mortgages. It is happening again.

#7 Just before the last financial crisis, unemployment claims started skyrocketing. Well, initial claims for unemployment benefits are rising again. Once we hit the 400,000 level, we will officially be in the danger zone.

#8 Continuing claims for unemployment benefits just spiked to the highest level since early 2009.

#9 The yield on 10 year Treasuries is now up to 2.60 percent. We also saw the yield on 10 year U.S. Treasuries rise significantly during the first half of 2008.

#10 According to Zero Hedge, "whenever the annual change in core capex, also known as Non-Defense Capital Goods excluding Aircraft shipments goes negative, the US has traditionally entered a recession". Guess what? It is rapidly heading toward negative territory again.

#11 Average hourly compensation in the United States experienced itslargest drop since 2009 during the first quarter of 2013.

#12 In the month of June, spending at restaurants fell by the most that we have seen since February 2008.

#13 Just before the last financial crisis, corporate earnings were very disappointing. Now it is happening again.

#14 Margin debt spiked just before the dot.com bubble burst, it spiked just before the financial crash of 2008, and now it is spiking again.

#15 During 2008, the price of gold fell substantially. Now it is happening again.

#16 Global business confidence is now the lowest that it has beensince the last recession.

#17 Back in 2008, the U.S. national debt was rapidly rising to unsustainable levels. We are in much, much worse shape today.

#18 Prior to the last financial crisis, Federal Reserve Chairman Ben Bernanke assured the American people that home prices would not decline and that there would not be a recession. We all know what happened. Now he is once again promising that everything is going to be just fine.

Are the American people going to fall for it again?

It doesn't take a genius to see how vulnerable the global economy is right now. Much of Europe is already experiencing an economic depression, debt levels in Asia are higher than ever before, and the U.S. economy has been steadily declining for most of the past decade. If you doubt that the U.S. economy has been declining, please see my previous article entitled "40 Stats That Prove The U.S. Economy Has Already Been Collapsing Over The Past Decade".

And the truth is that most Americans already know that we are in deep trouble. Today, 61 percent of all Americans believe that the country is on the wrong track.

It isn't that so many people are choosing to be pessimistic. It is just that an increasing number of Americans are waking up to the cold, hard reality that we are facing.

Decades of incredibly foolish decisions have brought us to this point. We allowed our economic infrastructure to be gutted, we consumed far more wealth than we produced, our politicians kept doing incredibly stupid things but we kept voting the same jokers back into office again and again, and over the past 40 years we have blown up the biggest debt bubble in all of human history.

We have been living so far above our means for so long that most of us actually think that our current economic situation is "normal".

But no, there is nothing normal about what we are experiencing. We are entering the terminal phase of a colossal debt spiral, and when it flames out the economic devastation is going to be absolutely spectacular.

When the next major wave of the economic collapse comes and unemployment soars well up into the double digits, millions of businesses close and millions of American families lose their homes, I hope that those that are assuring all of us that there will not be an economic collapse will come back and apologize.

There are tens of millions of people out there right now that are not making any preparations at all because they have been promised that everything is going to be okay. When the next financial crash happens, most of them will be absolutely blindsided by it and many of them will totally give in to despair.

Don't let that happen to you.

Be sure to listen to Financial Survival radio program live at dgscoins.com and Short-wave radio 7.490 AND 9.880Mhz M-F 4:00PM ET. We broadcast in cities of Spokane KTAC 93.0 5-6pm Eastern, Metairie WVOG 600AM 3-4PM Eastern and Dallas KXBD 1480AM 4-5PM Eastern.

Discount Gold & Silver Trading Co. provides all forms of precious metals including gold, silver platinum and palladium whether you are buying or selling. Our inventory includes but not limited to the American Gold, Silver, Platinum Eagle and numismatic products including rare, investment and circulated coins. Silver dollars, silver bars, rounds are on hand for the silver investor. Foreign gold is also available. Call for information regarding your precious metal gold and silver IRA. Call 1-800-375-4188 or visit the Web site at dgscoins.com or email us at: discountgoldandsilver@yahoo.com

1-800-375-4188

Health

Neutralize what is lethal

by Herbalist Wendy Wilson

We live in toxic times. Most of us don't live healthy lives; we drink, we smoke, we take pain medication for everything, we eat more chemicals than any generation before and that's just the physical toxicity. Add some post-traumatic stress disorder, ADHD, depression and adrenaline junkies and if the liver could it would divorce us. So, let's do something nice for our abused bodies and check out a mineral that can offer some serious relief.

MAGNESIUM

Most of us have heard about magnesium and that bananas offer the nutrient. However, magnesium is more important than we could have ever thought. It not only assists with function but also the structure of the human body. Our bones contain 60% of the magnesium in our body, 27% is in our muscles, 7% is inside the cells and 1% is outside the cells.

WHY SO IMPORTANT?

We have 300 metabolic functions relying on this mineral. If you want to relax, this is the mineral you want as it is known as the anti-stress mineral. Magnesium will relax muscles (including the heart), assists in enzyme function, protein synthesis, energy production and neuromuscular function. For hundreds of years foods, spices and herbs containing magnesium were used to calm anxiety, improve sleep, diminish menstrual cramps, muscle spasms, reduce blood pressure, defuse asthma attacks and normalize heartbeat. Magnesium is the architect of bone structure. It is needed to help transport other nutrients such as calcium, potassium and boron to cells. While it is doing all that, magnesium also helps with the conduction of nerve impulses in order for muscles to contract and for your heart to keep beating. Magnesium has a role in the way the body utilizes zinc, fiber, protein, calcium and vitamin D.

DEFICIENT

Usually is it rare to have a magnesium deficiency because our kidneys help to manage levels so we don't secret too much and it is in so many food sources such as green leafy vegetables, nuts, seeds, grains, beans and seafood. However, those with low calcium also have low magnesium levels in the body. You won't find the adequate magnesium and calcium you seek in dairy products. The dark green vegetables will be an excellent source of magnesium as it pairs with the chlorophyll to store usable energy for the body and for oxygen-rich hemoglobin. If there is a deficiency it will usually create gastrointestinal disorders such as acute diarrhea, Crohn's disease, celiac disease (auto immune gluten intolerant), renal (kidney) problems and diabetes.

OTHER CAUSES

Some other causes that will create a magnesium deficiency are alcoholism, drugs for diabetes, diuretics and other drug interactions. You can avoid many health problems with organic magnesium such as heart disease, osteoporosis, high blood pressure, preeclampsia (toxemia pregnancy), heart attacks, vascular disorders, diabetes, asthma and migraine headaches.

DRUG INTERACTIONS

Magnesium can interfere with the absorption of some prescription drugs and should not be taken at the same time. Drugs such as; heart meds (digoxin), antibiotics, anti-malarial drugs and osteoporosis drugs. Physicians will tell patients to space the administration of magnesium supplements two hours after taking their drugs. http://lpi.oregonstate.edu/infocenter/minerals/magnesium/

DETOX MINERAL

There is a lot of great nutritional information about magnesium and research seems to indicate that it also helps protect us from lethal toxins. A study in the Journal of Experimental Medicine published in 1918 showed that magnesium can restore the body after exposure to lethal substances. In a nut shell the scientists used rabbits and injected them with lethal doses of sodium oxylate (very fast 100% mortality rate). Some rabbits also received an immediate dose of magnesium .The rabbits receiving the magnesium had an 80% survival rate. The research showed that magnesium neutralized the toxins while supporting the immune system function. RESTORATIVE EFFECT OF SALTS OF MAGNESIUM AND CALCIUM AFTER LETHAL DOSES OF SODIUM OXALATE.

CONTENT WITH TOXICITY

There is no reason to be toxic when we have the natural answers all around us in our food and herb sources. Herbs such as red clover, burdock root, yellow dock and chaparral have very high magnesium content. Blue green algae such as chlorella and spirulina also are an excellent source of magnesium. http://articles.mercola.com/sites/articles/archive/2012/02/01/is-this-one-of-natures-most-powerful-detoxification-tools.aspx So there is no reason to be content with toxicity even if you are not able to eat as healthy as you should. You can supply your body with an organic source of magnesium which will have the required uptake nutrients for the body to utilize properly.

EMPOWER YOURSELF

For hundreds of years mankind has relied on natural nutrients in foods and herbs to help restore balance and destroy deadly toxins. You have this power today and it doesn't require an insurance card, a deductible or co-pay to obtain it. Detoxing has never been easier than with the organic products and instructions provided by Apothecary Herbs. Call them today to see just how simple and effective it can be to remove heavy metals, pharmaceutical residues, radio active particles and more. Their Body Foundation Food mix contains the spirulina and chlorella for magnesium potency as well as many of their organ cleanses to help the body heal itself. For a perfectly balanced magnesium and calcium source look for their herbal Calcium Formula. Call now to order 866-229-3663, International 704-885-0277 online http://www.thepowerherbs.com, where your healthcare options just became endless. Our subscribers receive special discounts at Apothecary Herbs. Take advantage of coupon code VP2013 and receive 15% off your order. Hurry! Coupon expires 7/31/2013. Fall is just around the corner – use your discount coupon to stock up and SAVE!

MORE HERB SECRETS IN THE POWER HERBS e-BOOK. By popular demand The Power Herbs e-book is available with symptom/herb reference guide, information on organ cleansing and how to make your own herbal tinctures plus a whole lot more. Go to http://www.thepowerherbs.com/Books-And-Newsletters/The-Power-Herbs-e-Book-cleansing-immune-boosting.html and click on Books. You must have email to order and receive the e-book a PDF version of The Power Herb book for just $14.99. At this time, we do not offer this title in hard copy.

COMING UP ON HERB TALK LIVE

Herbalist Wendy Wilson on Herb Talk Live

Saturday morning show:

7 am EST on GCN

8/10/13 Dr. Rebecca Carley

Weekday show:

7 pm EST on AVR

8/13/13 Dr. Paul Kinsinger on natural nail fungus cures

8/20/13 Dr. Rebecca Carley

Shortwave show 8 pm EST WWCR 4840

Go to http://www.thepowerherbs.com/archive.html Herb Talk Live & Radio Archive area for network link access and past shows to download and share. For Android users you can download a FREE app for Herb Talk Live on GCN. See the download link under radio archives at top of page.

The information contained herein is not designed to diagnosis, treat, prevent or cure disease. Seek medical advice from a lincensed medical physician (if you dare) before using any product or therapy.

|

|

| |

|